The Wake-Up Call: Why Retirement Planning Can’t Wait

Picture this: You’re in your late 50s, sitting in a cozy beachside cottage, sipping your favorite beverage, and watching the waves roll in. Life is peaceful because you made the right financial decisions early on. Now, let’s rewind to your 20s and 30s—when most people think they have all the time in the world to start saving for retirement.

The truth is, the earlier you start, the better your future will look. Yet, many people delay saving because retirement feels like a distant dream. However, time is your biggest asset. With the power of compounding, small contributions today can grow into a significant nest egg tomorrow.

The Power of Starting Early: A Tale of Two Friends

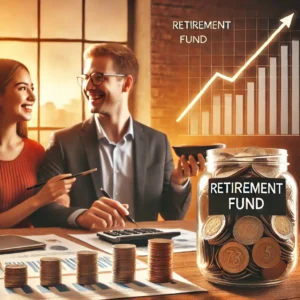

Meet Rahul and Sameer, two college friends who start their careers together at age 25. Rahul begins investing $200 per month into a retirement fund, earning an average annual return of 8%. He does this for 10 years and then stops contributing but leaves the money invested.

On the other hand, Sameer waits until he’s 35 to start saving. He contributes $200 per month until he retires at 60. Even though he invests for 25 years, Rahul ends up with more money at retirement—thanks to compound interest!

This example illustrates why starting early is crucial. The longer your money stays invested, the more it grows.

Step 1: Define Your Retirement Goals

Before you start saving, ask yourself a few questions:

What kind of lifestyle do you want in retirement?

At what age do you want to retire?

Do you want to travel, own a vacation home, or start a business?

Having a clear vision helps you determine how much you need to save. Financial experts recommend saving at least 15% of your income for retirement. But if you start late, you may need to contribute more to catch up.

Step 2: Take Advantage of Employer Benefits

If your company offers a retirement plan like a 401(k) (or EPF/NPS in India), enroll as soon as possible. Many employers match contributions up to a certain percentage—this is free money that boosts your savings! If your employer matches 5% of your salary, ensure you’re contributing at least that much.

For freelancers or those without an employer-sponsored plan, consider options like:

IRA (Individual Retirement Account) in the U.S.

PPF (Public Provident Fund) or Mutual Funds in India

Robo-advisors for automated investing

Step 3: Automate Your Savings

One of the easiest ways to save consistently is automation. Set up automatic transfers from your paycheck to your retirement account. This method ensures that you prioritize savings before spending on non-essentials.

Think of it as a ‘set and forget’ strategy. Once the money is out of sight, you won’t be tempted to spend it.

Step 4: Invest Wisely for Long-Term Growth

Your 20s and 30s are the best time to take investment risks because you have time to recover from market downturns. Here’s how you can structure your investments: Always go with proper financial advisors. Even this article gives overview and not how to invest as everyone`s need and requirements will be different.

Stocks & Mutual Funds: Historically, stocks offer higher returns over the long run. Consider index funds, mutual funds, or ETFs to diversify your portfolio.

Retirement Accounts: Max out contributions to retirement accounts first before investing elsewhere.

Real Estate: If possible, invest in property for long-term wealth-building.

Remember, investing doesn’t mean gambling. Do your research and seek expert advice if needed.

Step 5: Cut Unnecessary Expenses and Save More

If you think you don’t have enough money to save, track your expenses. Small changes can make a big difference:

Cook at home instead of ordering takeout.

Skip that extra coffee run.

Use public transport or carpool instead of buying a new car on EMI.

Cancel subscriptions you don’t use.

Redirect these savings toward your retirement fund. Over time, these small sacrifices add up significantly.

Step 6: Stay Out of Debt for early retirement

Debt can derail your retirement plans. Prioritize paying off high-interest debts like credit cards and personal loans. The less money you owe, the more you can invest in your future.

A good rule of thumb is to maintain a balance between saving and debt repayment. Avoid lifestyle inflation—just because your salary increases doesn’t mean your expenses should skyrocket.

Step 7: Increase Contributions Over Time

As your income grows, increase your savings rate. If you get a bonus, raise, or unexpected income, direct a portion of it into your retirement fund. The goal is to reach a point where you’re saving at least 20-25% of your income.

Step 8: Have an Emergency Fund

An emergency fund (3-6 months’ worth of expenses) ensures that you don’t dip into your retirement savings during a crisis. Keep it in a liquid, accessible account like a high-yield savings account or fixed deposit.

Real-Life Example: The Couple Who Retired at 40

Ramesh and Priya, a middle-class couple, started saving aggressively in their 20s. They lived modestly, invested wisely, and avoided unnecessary expenses. By the time they hit 40, they had accumulated enough wealth to retire early and travel the world. Their strategy?

Investing 50% of their income.

Living in a smaller home instead of upgrading.

Side hustles for extra income.(Not necessary that everyone needs this, one can focus on one important thing to go deep as well)

Their story proves that disciplined saving and smart investing can make early retirement a reality.

Final Thoughts: The Best Time to Start is Now

It’s easy to put off retirement planning when you’re young. But the best gift you can give your future self is financial security. Whether you start with $50 or $500 a month, consistency is key.

Your 20s and 30s set the foundation for a stress-free retirement. So, take action today—your future self will thank you.

Here are some useful links that you support for further reading and resources:

-

Retirement Planning Basics – Investopedia

-

Power of Compound Interest – NerdWallet

-

Best Retirement Investment Options – Morningstar

-

How to Budget and Save for Retirement – Forbes

-

Retirement Planning for Young Professionals – The Balance

-

401(k) and IRA Contribution Limits – IRS.gov

-

National Pension System (NPS) for Indian Investors – NPS Trust

-

Best Mutual Funds for Retirement in India –Moneycontrol

TOP 5 investing books for all the time

For more understanding in finance. Visit our Finance section